James Stewart: The commission assessment of unpaid taxes at €13bn plus interest, to be recovered by Ireland is much higher than most expected, especially the Government.

However, the commission also note that the amount that may be recovered by Ireland will be much lower if as a result of information “revealed through the commission’s investigation” profits are reallocated to other jurisdictions. There is a precedent for such a reallocation, in the case of Italy.

In addition, the commission note the amount recovered by Ireland would also be reduced if larger sums were reallocated to the US parent to “finance research and development”.

Thus the commission envisage a considerable international reallocation of profits attributed to the Irish Apple subsidiaries. This in itself will result in investigations by various revenue authorities and possible court cases.

The Irish Government has also maintained that an adverse ruling would be appealed and this was reaffirmed after the commission decision.

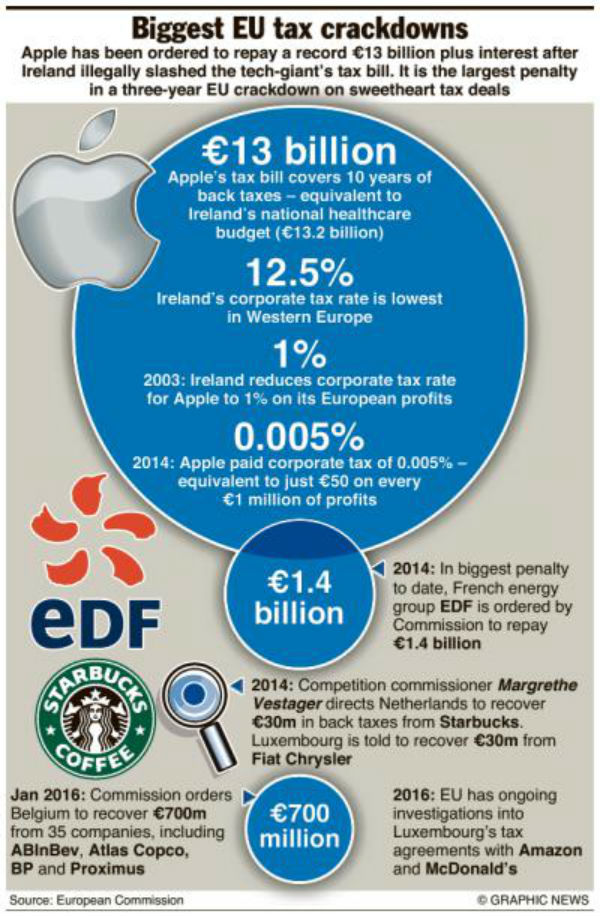

Given the costs involved for the taxpayer in the Government engaging in a protracted and costly appeal process (about €700,000 has been spent and court appeals could cost several million more), and lack of clarity as to precisely why this decision is being appealed, it is important to assess the likelihood of a successful appeal.

The US Treasury recently (August 24, 2016) published a white paper on recent EU decisions in relation to competition decisions on illegal state aid. This document is highly critical of EU policies in relation to State aid.

Effectively, the US government is acting as an advocate on behalf of affected US companies and has devoted considerable resources to setting out the case against the commission in relation to three recent decisions involving illegal State aid.

The grounds set out in the white paper (though brief — 25 pages) are the likely arguments which may be used by the Irish State. Hence it is useful to examine these arguments and assess whether they have any merit and justify extensive legal costs.

What is the US case?

It is important to remember that the reason the commission initiated the Apple case was because of a US Senate sub-committee inquiry into Apple Ireland which drew attention to the fact that Apple earned about 60% of its global profit in Ireland and paid virtually no tax on these profits because Apple had no tax residency in any jurisdiction — an example of “double non-taxation”.

There are several strands to the US case, some consist of mere assertion, others are based on interpretations of what has been agreed by the G20 and OECD as to the nature of international tax reform, some are based on interpretations of European law.

Others are purely self-interest, for example that one effect of commission decisions would be to increase corporate tax receipts in certain EU countries, giving rise to additional tax credits and hence a reduction in US corporate tax revenue.

The overall conclusion of the white paper is not, however, based on legal or economic arguments, or arguments about necessary tax reforms but rather a threat. The white paper states: “The US Treasury Department continues to consider potential responses should the commission continue its present course.”

It also states: “Recovery of past, allegedly unpaid tax would constitute retroactive enforcement of a newly adopted approach to State aid”, and “as a general matter, retroactive enforcement runs counter to one of the fundamental principles of EU jurisprudence: the principle of legal certainty.”

Retrospective recovery is in fact a long established principle in relation to cartel cases (and sometimes for very large amounts), taken by the directorate general for competition.

Retrospective recovery is also a long established principle of tax law where a particular tax or elements of a tax strategy has been found by the courts to be illegal. The white paper states: “The commission has suggested that it may also become an arbiter of tax settlements agreed to by member states with taxpayers.”

The case referred to is the agreed settlement between the UK government and Google. The commission became involved only after a complaint from the First Minister and leader of the SNP in Scotland.

The competition directorate may often inititate investigations following complaints. Indeed, US firms are sometimes the initiator of these complaints as in the complaint by Microsoft against Google in relation to the dominance of the Google search engine.

The white paper makes much of the principle of certainty (referred to 13 times). For example, the white paper states that retrospective taxation would undermine “G20’s efforts to improve tax certainty”.

However, the main tax reforms agreed in the OECD BEPS proposals (and agreed by the US) relate to issues such as preventing double non-taxation of which the Apple case is the most notorious.

The effect on the US tax revenues

The white paper states: “There is the possibility that any repayments ordered by the commission will be considered foreign income taxes that are creditable against US taxes owed by the companies in the United States.

“If so, the companies’ US tax liability would be reduced dollar for dollar by these recoveries when their offshore earnings are repatriated or treated as repatriated as part of possible US tax reform.”

However, this statement fails to recognise that US companies currently earn a majority of their profits overseas but pay most of their corporate taxes in the US. Irrespective of what the commission decides increasing the tax take on overseas profits will generate tax credits that can be used to reduce tax payments in the US.

There are, of course, issues relating to the interpretation of law. For example, the white paper states: “First, it appears that the commission has collapsed the concepts of ‘advantage’ and ‘selectivity’, which are distinct requirements under state aid law.

“In the state aid cases, the commission simply examined whether the measures at stake conferred a ‘selective advantage’ on the companies under investigation, rather than separately assessing the existence of an advantage and the selective character of the measure, as it had done in prior decisions.”

This distinction does not appear to be central to the commission case. In particular, in the Apple case, the tax ruling was selective in that it appears very few firms obtained this benefit and it was certainly to the advantage of Apple.

What should the commission do?

Commission actions in relation to illegal state aids are one of the (unfortunately) few areas of commission policy that have the overwhelming support of EU citizens. The Competition Directorate is one of the few areas that interested citizens and their representatives can appeal over the heads of government to act in the public interest rather than narrow sectional interest (as in the Google case referred to earlier).

In contrast, the actions of the US and Irish governments in acting as an advocate for Apple to oppose commission policy are not in the public interest.

The Competition Directorate deserves the support of all EU citizens in continuing to pursue policies to eliminate illegal State aid and redress the balance between corporate power (often supported by governments) at the expense of citizens’ rights.

The grounds for an appeal appear very weak and may simply represent a vanity project (“we have done nothing illegal”) or may reflect an implicit contract that not only will the Irish State grant tax expenditures/favourable tax regime, but will incur considerable State expenditures to protect the benefits to selected firms.

In conclusion, this decision should not be appealed. These tax rulings, once made public by the US Senate investigation were not sustainable, and Irish tax law has been amended to ensure that firms cannot be stateless.

Appealing this decision gives the appearance that Ireland considers that the tax regime that Apple benefitted from was legitimate.

Prof James Stewart is associate professor in finance at Trinity College Dublin

This article was published in the Irish Examiner, Wednesday 31st August, 2016

Share: