Rory Hearne: The increasing concentration of wealth at the top of society has become a major economic, social and political issue. It is surprising, therefore that last week’s Knight Frank Wealth Report 2016, which suggests that the number of ultra-wealthy individuals in Ireland is set to increase by 28% over the coming decade, did not garner more attention.

The Wealth Report 2016 (see here) finds that the number of ‘ultra high net worth’ (UNHW) individuals in Ireland increased by almost a fifth since 2005 (increasing from 712 to 840) with the number set to increase by 28% to 1075 by 2025. Table 1 reproduces the key data on wealth distribution for Ireland from the Report. These UHNWs are defined as having a net worth of at least US$30 million (after accounting for shares in public and private companies, residential and passion investments such as art, planes and real estate). The Report also finds that the number of millionaires in Ireland is projected to increase from 66,000 in 2005 to reach 100,400 by 2025.

Table 1 COUNTRY-LEVEL WEALTH DISTRIBUTION: Ireland | |||

2005 | 2015 | 2025 | |

No. of Ultra High Net Worth Individuals ($30m+) | 712 | 840 | 1,075 |

Millionaires ($1m+) | 66,400 | 78,400 | 100,400 |

Centa-millionaires ($100m+) | 76 | 90 | 115 |

Billionaires ($1,000m+) U | 4 | 5 | 6 |

UHNWI % change | 2005- 2015 | 2015-2025 | |

+18% | +28% | ||

Source: Knight Frank Wealth Report 2016

The Knight Frank Wealth report follows on from the recent Sunday Independent Rich List which showed that the top 300 wealthiest Irish people doubled their wealth since 2010. Analysis of their figures shows that these top 300 have €87.7bn in wealth.

There is a stark contrast between this rising wealth for those at the top of Irish society and the reduction in wealth and income for those in the middle and at the bottom. For example, in terms of deprivation, in the same period of time as covered by this increase in wealth, the number of children aged 0-6 suffering from deprivation in Ireland doubled from 55,000 in 2007 to 105,000 in 2014.

TASC’s recent paper, ‘The Distribution of Wealth in Ireland’, based on the CSO Household Finance and Consumption Survey, found that half of all the people in Ireland have less than 5% of the wealth in the country while the top 20% have 70% of the net wealth. It also found that wealth inequality has been increasing over the last three decades.

The Knight Frank Wealth Report is particularly interesting and important for the Irish context of a worsening housing crisis and the accumulation of wealth by property investors and vulture funds through the on-going financialisation of housing. The Wealth Report focuses on property (residential and commercial real estate property) as a key aspect of ‘wealth creation’ (as they term it - of course it is more accurate to describe it as wealth ‘accumulation’). They highlight that “super-normal” returns” experienced by those holding residential property “helps underpin the net worth of the ultra-wealthy” and, therefore, “the Wealth Report has documented the performance of prime property and its interaction with wealth creation.”

Knight Frank themselves are a global ‘property agent’ and property advisor, handling sales of very large properties. Clearly, promoting the role of property in wealth accumulation for UHNW individuals is an important aspect of their business model.

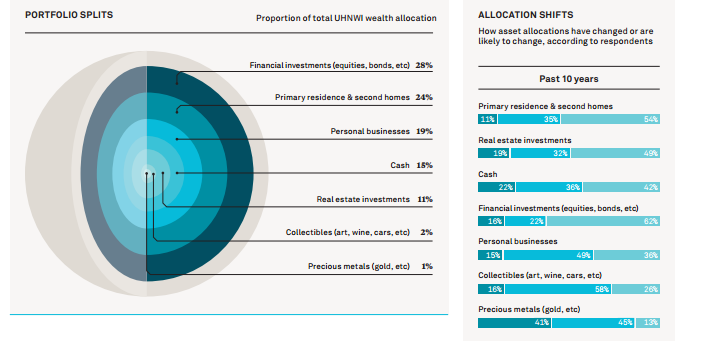

Their Report shows that housing property (primary residence and second homes) accounts for a quarter of UHNW’s investable wealth, while commercial property investments make up 11%. Thus, total property investment makes up almost 40% of the wealth of the UHNWs while financial investments (equities, bonds, etc) makes up a smaller proportion (28%). And the importance of property as an asset has increased in recent years with 54% increasing their allocation to residential property in the last 10 years. This contrasts to just 16% increasing their allocation to their personal business (see Figure 1). The reason for the increasing importance of purchasing property was its role as an ‘investment to sell in the future’ and a ‘safe haven for funds’.

Figure 1: Where the wealthy invest their funds

Source: Knight Frank Wealth Report 2016

In terms of property price increases in ‘prime’ markets (such as Dublin) they point out that “it has been the weight of money from wealthy investors looking to secure assets in leading world economic hubs that has propelled markets to record levels”. They also note that there is “increased attention being paid by governments on the impact rising investor demand for residential property is having on affordability in key urban markets”. I have highlighted the role of global wealth funds in previous TASC blogs (see here) in worsening the housing affordability crisis in Ireland by driving up rents through the sale of property and land by NAMA to vulture funds.

This is the necessary ‘other side’ of the same coin of property based forms of wealth ‘creation’ (accumulation). It is, as the critical political economist David Harvey has accurately described, ‘accumulation through dispossession’. The vulture funds and banks increase their wealth by dispossessing the poorest of their homes and extracting surplus value or ‘super profit’s from speculative sales of land and property, along with rental income. This wealth isn’t created from thin air – it is being accumulated from losses paid for by the Irish taxpayer through the bank bailouts, austerity and NAMA, mortgage distress and escalating rents and house prices.

The result of this is most visible in our housing crisis –from the 37,000 still in mortgage arrears to the 1,570 children and their families who are now homeless in Dublin.

Figure 2 The worsening homeless crisis in Dublin

It is interesting to read in the Report that even the wealthy are realising that the growing concentration of wealth, particularly within the advanced economies, is a major problem. There is a specific Chapter in the Report entitled ‘Wealth Inequality takes Centre Stage’ which highlights the ‘growing sense of disenfranchisement” that “is changing the political landscape globally”. They explain:

“wealth inequality has continued to climb the political agenda and is now one of the biggest issues facing politicians as they try to address those who feel disenfranchised. Ultimately, feelings of social, economic and political inequality can ferment revolution, as in the case of the Arab Spring. The electorates in Western economies have also been making their feelings known, with the rise of populist right-wing politicians in the US, France and Hungary, while in the UK, the opposition Labour party has made a significant jump to the left with the election of Jeremy Corbyn as party leader.”

There is also some discussion of various proposals for addressing wealth inequality with reference to Thomas Picketty and wealth taxes and the recent IMF paper highlighting that “better access to education and health care and well-targeted social policies…can help raise the income share for the poor and middle class.” It is the report’s view that “higher taxes, curbs on foreign investment and loan caps will continue to spread globally.” Although in Ireland we have seen tax breaks (rather than tax increases) introduced for global wealth funds such as Real Estate Investment Trusts.

The report also highlights the remarkable growth in cross-border capital flows and investment by individuals and Ireland’s significant role in this. Their graph (reproduced below - Figure 3) shows Ireland in the incredible position of having greater ‘outward investment’ (assets that are claims of a local resident on an asset located in a foreign country) than Brazil, Italy or Russia. One would expect the management of funds from the IFSC (with Ireland’s low tax regime) being a significant factor in explaining this. This once again highlights the likely role of Ireland’s low tax regime in facilitating the further wealth accumulation of the rich and corporations and rising wealth inequality both in Europe and globally.

Figure 3 Shift in global wealth movements

The data for UHNW individuals in Knight Frank’s Wealth Report is gathered from 400 of the “world’s leading private bankers and wealth advisors who, between them, manage assets for about 45,000 ultra-high-net-worth individuals (UHNWIs) with a combined wealth of over half a trillion US dollars”. They undertake the survey with the (scarily named!) ‘ultra-wealth intelligence consultancy – Wealth X’. Wealth X’s website states that it provides “wealth managers, family offices, hedge fund companies, and investment and corporate bankers with in-depth intelligence on UHNW customers and prospects”.

Clearly these are people who would have a fair idea of the true extent of the wealth held by the UHNW individuals. But does that mean the information presented in the report is accurate? Or is it what the wealthy want us to know? There is a major issue about the accuracy of data on wealth because of the lack of transparency in the declaration of ownership of property and assets (including company and financial investments). It is expected that the wealthy tend to understate their wealth (for obvious reasons – reducing tax, public and political attention). So maybe the health warning for this data should be that these are likely to be underestimations of the true extent of UHNW individuals. The wealth analysis undertaken by TASC of the CSO data is a more reliable source of information but unfortunately it does not break down to the level of UHNWs.

Co-incidently, in terms of the debate about how to address the problems associated with rising wealth inequality, the Irish Times journalist Diarmuid Ferriter reminded us yesterday that it was a Fine Gael Labour government which introduced a wealth tax in Ireland in 1975. It was levied at 1 per cent of the value of assets in excess of £100,000, with family homes, bloodstock, livestock and pension rights exempt. But after the 1977 election, Fianna Fáil abolished the wealth tax.

TASC’s research shows that if a 1% wealth tax on net assets in excess of €1 million (which would apply therefore only to the top 1% of households in Ireland) was introduced today it would have a yield of approximately €500 million (TASC 2013 Wealth Tax). NERI have similarly found that a wealth tax of 0.5% which excluded people’s homes, farm land, people’s vehicles and people’s pension savings could raise approximately €400 million per annum for the exchequer. Such a tax would fall on wealth in the form of investments in property, shares and bonds alongside business assets and savings. Thus the introduction of a wealth tax would provide a significant annual sum of money that could go a long way to address the housing crisis.

This again highlights the importance of progressive taxes, such as a wealth tax. They can reduce the levels of inequality through the provision of funding that can address key social inequalities such as the housing and homeless crisis currently affecting growing numbers of families in Ireland.

Dr Rory Hearne is a Senior Policy Analyst at TASC. You can follow him on twitter @RoryHearne

Dr Rory Hearne @RoryHearne

Rory Hearne is a postdoctoral researcher in the Maynooth University Social Sciences Institute (MUSSI), working on the Re-Invest Participatory Action Human Rights and Capability project in relation to social investment with a particular focus on homelessness and water infrastructure.

He has a PhD in political and economic geography from Trinity College Dublin. He is also a former policy analyst with TASC and has worked as a policy researcher and community development worker with Barnardos on social housing regeneration and human rights in Dublin's inner city. He was lecturer in human geography in the Department of Geography, Maynooth University and has researched and published extensively in the areas of housing and social housing, political economy, human rights, social movements, and politics.

He is author of Public Private Partnerships in Ireland (2011) and co-author of Cherishing All Equally (2016). He is also a regular economic and social analyst on various national media.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)