Robert Sweeney: As the election season reaches full swing, the inevitable claims of who did what and when, and what this means in the future intensifies. One oft-repeated tale beginning to reemerge is that an expansion in public spending during the 2000s is a, or perhaps the, leading cause of the subsequent financial and debt crisis. After all, as seen below, the crisis manifested itself in an explosion of the public deficit and overall debt, which eventually culminated in an inability of the government to borrow from financial markets in 2010.

While the topic has been much-discussed, it’s worth going over this again as there are several misunderstandings, and some questions which I think progressives and the left have had difficulty answering too.

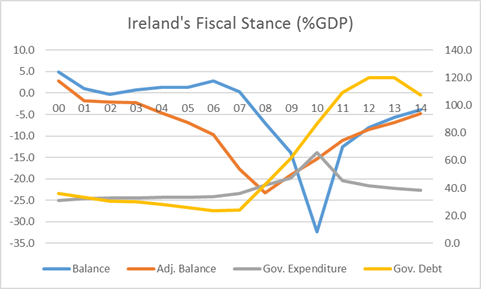

Notes on graph: The Fiscal Balance and Adjusted Balance are shown on the left-hand side, Expenditure and Debt are shown on the right-hand side. Adjusted Balance taken from IMF’s World Economic Outlook. All others are taken from Eurostat.

The most obvious counter to the argument that bloated public spending was at the centre of the crisis is to point out the actual trajectory of fiscal policy in the 2000s. As shown above, Ireland actually ran a surplus (blue line) in all but one year of the 2000s pre-crisis, and also had one of the lowest debt-to-GDP ratios in the developed world. As a proportion of national income, spending essentially stagnated. Thus, if anything, it was a model of fiscal prudency.

The counter to this is that, yes, the headline deficit was actually a surplus, but this masks underlying structural weaknesses. As we all know by now, the surpluses arose because of transient taxes such as stamp duty and other bubble-related windfalls. There was an expansion in public spending and the headline surplus was in reality a deficit (or as economists would say there was a structural public deficit). This was hidden by a basket-case economy, which delayed the inevitable collapse. In reality, the state was spending money it didn’t have - government profligacy in the form of excess spending has been a root cause of our woes. This can be seen clearly by the evolution of the cyclically-adjusted government balance, which clearly shows a large deficit from 2001 on.

Progressives and those on the left have difficulty answering this, and as a result it weakens the case for greater public investment in services, infrastructure, and so on. One response is to point to the costs of the bank bailout. Another is to repeat the point that the public finances were in surpluses. Another criticism is that it is in practice impossible to measure a structural deficit: that is, one cannot disentangle structural versus cyclical components of the deficit. I think all of these answers are somewhat weak, and leave open the charge of denial.

While the bank bailout did, of course, hugely exacerbate the public deficit/debt, it has been quite convincingly shown that most of it is independent of the bailout, at least directly. Second, as noted, to point to public surpluses in the 2000s does not address the fact that much of this spending was based on transient revenues. Finally, while a structural deficit may be deeply flawed and in practice unmeasurable, it is surely valid as a concept.

The point of the matter is that, yes, public spending was to a significant degree based on unsound revenue sources which were unaffordable in the long run (at the prevailing level of taxation). But to argue that this was a result of public profligacy presupposes an awareness of bubble. In fact, given the prevailing belief at the time that economy’s fundamentals were sound, fiscal policy was actually conservative. There is simply no good economic reason to run a 3% budget surplus with a public debt-to-GDP ratio of well under 30% and an inflation rate of less than 3%, as was true in 2006. This is especially true if there are infrastructural and other deficiencies. Moreover, successive governments have shown little reluctance to impose severe cuts to balance the books, so the idea that the collapse in public finances can be explained away by the buying of elections through giveaway budgets is also fallacious. All the evidence points that if the emerging hole in the coffers had been seen, this would have been quickly (and ruthlessly) addressed.

Thus, the most coherent explanation for the collapse in public finances was that there was a housing bubble which policymakers failed to see. In so far as there was recklessness, this was not so much on the public spending side as it was on the belief in the merits of financial deregulation.

Robert Sweeney @sweeneyr82

Robert Sweeney is a policy analyst at TASC and focuses on issues surrounding Irish political economy and distribution. He has a PhD in economics from University of Leeds, which concentrated on financial markets and investors, banking, international macroeconomics, and housing. He is also interested in debates on alternative schools and methodology in economics, and ownership.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)