Cormac Staunton: As reported in the Irish Times, the government is considering introducing “tax benchmarking” for income tax in order to attract emigrants to come home – particularly from Anglophone countries such as the UK, the US, Canada and Australia.

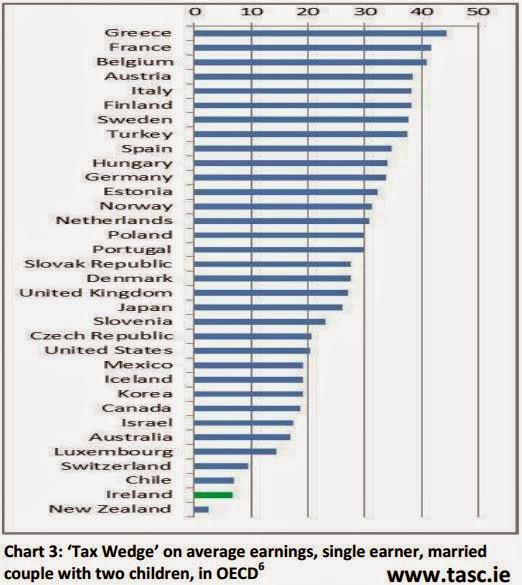

The implication is that our income tax system is a major barrier for people to return to Ireland, particularly for those on average earnings. If this were true (and there is little evidence that it is) it would be very odd; because Ireland has one of the lowest rates of tax on average earnings in the OECD:

So what is going on?

Well, from the Minister's statements there seems to be a focus on reducing the ‘marginal’ rate of tax.

“If you take the tax rate that a young Irish professional or a young Irish building worker pays in London, they won’t go into the higher rate until they are at in excess of £150,000 (€190,000), they go into the higher rate here at €32,800.” (Minister Noonan, Summer 2014)

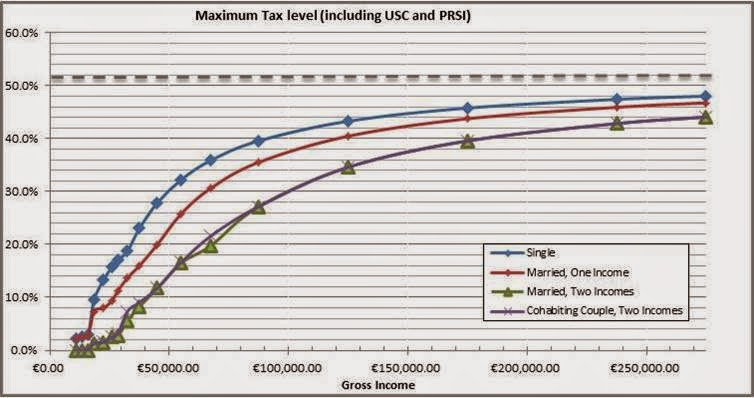

Comparing marginal rates is the wrong way to compare tax systems. They are only one cog in a huge and complex machine. There can also be significant difference between marginal rates (the ‘headline’ rate) and the effective rate (what you actually pay).

To understand why Ireland's marginal rate appears high while our effective rates are low, and why the highest marginal income tax rate is at average earnings, there are two important considerations to note:

The first is tax credits. In Ireland, credits essentially put a zero rate of tax on the first €16,000 for a single person (more for a married couple with one income). What this means is that if you earn €32,000 a year (and are paid monthly) then each month you essentially pay no tax for the first two weeks, and 20% for the next two weeks. Your marginal rate of income tax is 20%. But your effective rate is 10% (USC and PRSI are added too, but the idea is the same).

It looks like this (2014 data)

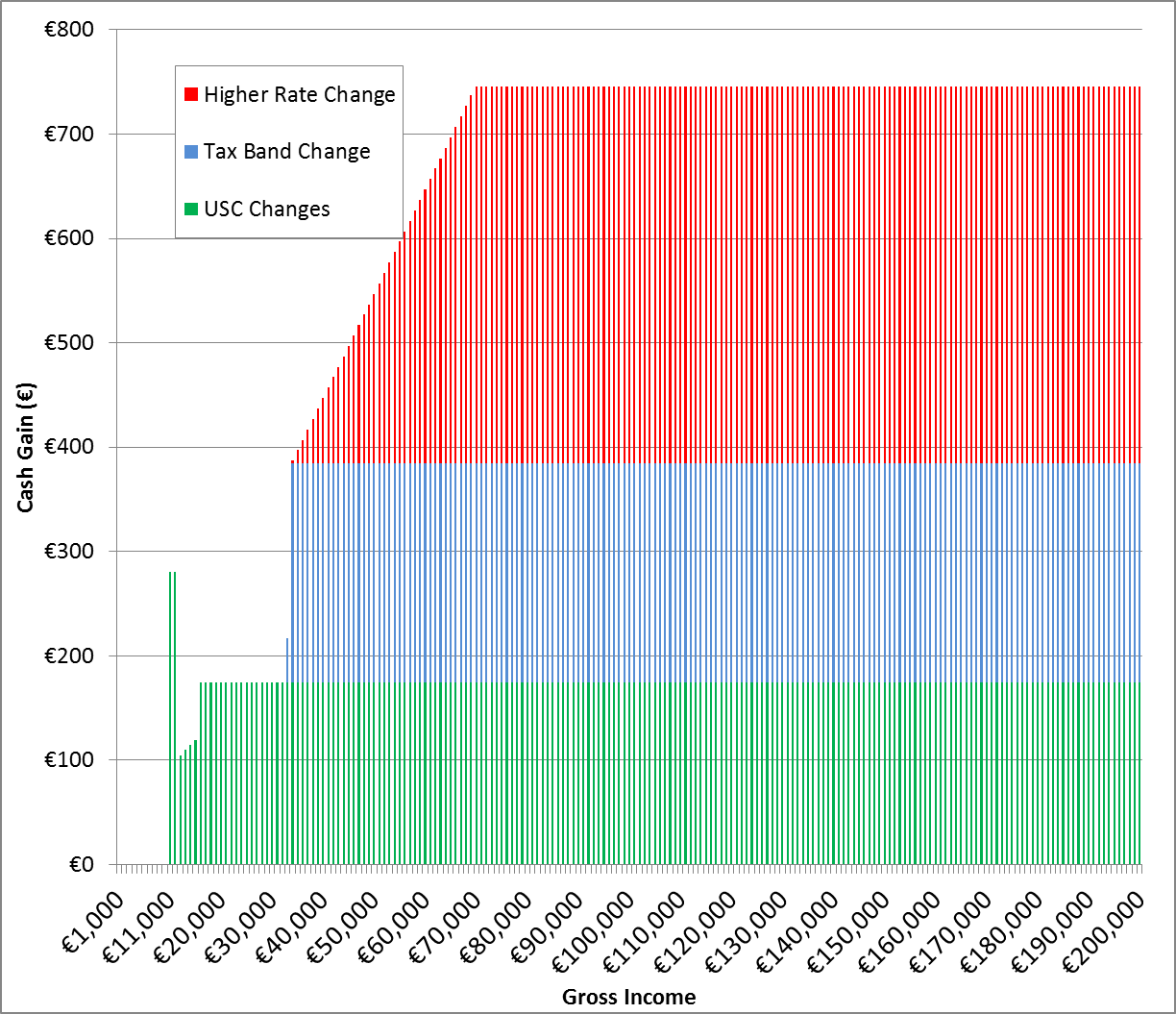

Secondly, Ireland only has two rates of income tax (we have more of USC). Prior to Budget 2015, this meant that the highest marginal rate was at €32,800 (Due to changes in the Budget our highest marginal rate is now at €70,000 - where we have the highest rate of USC). The reason the UK’s marginal rate is higher again is because they have a third rate of income tax on earnings over £150,000. Ireland could introduce a third rate of income tax at €100,000 and the highest marginal rate would then be at three times average earnings.

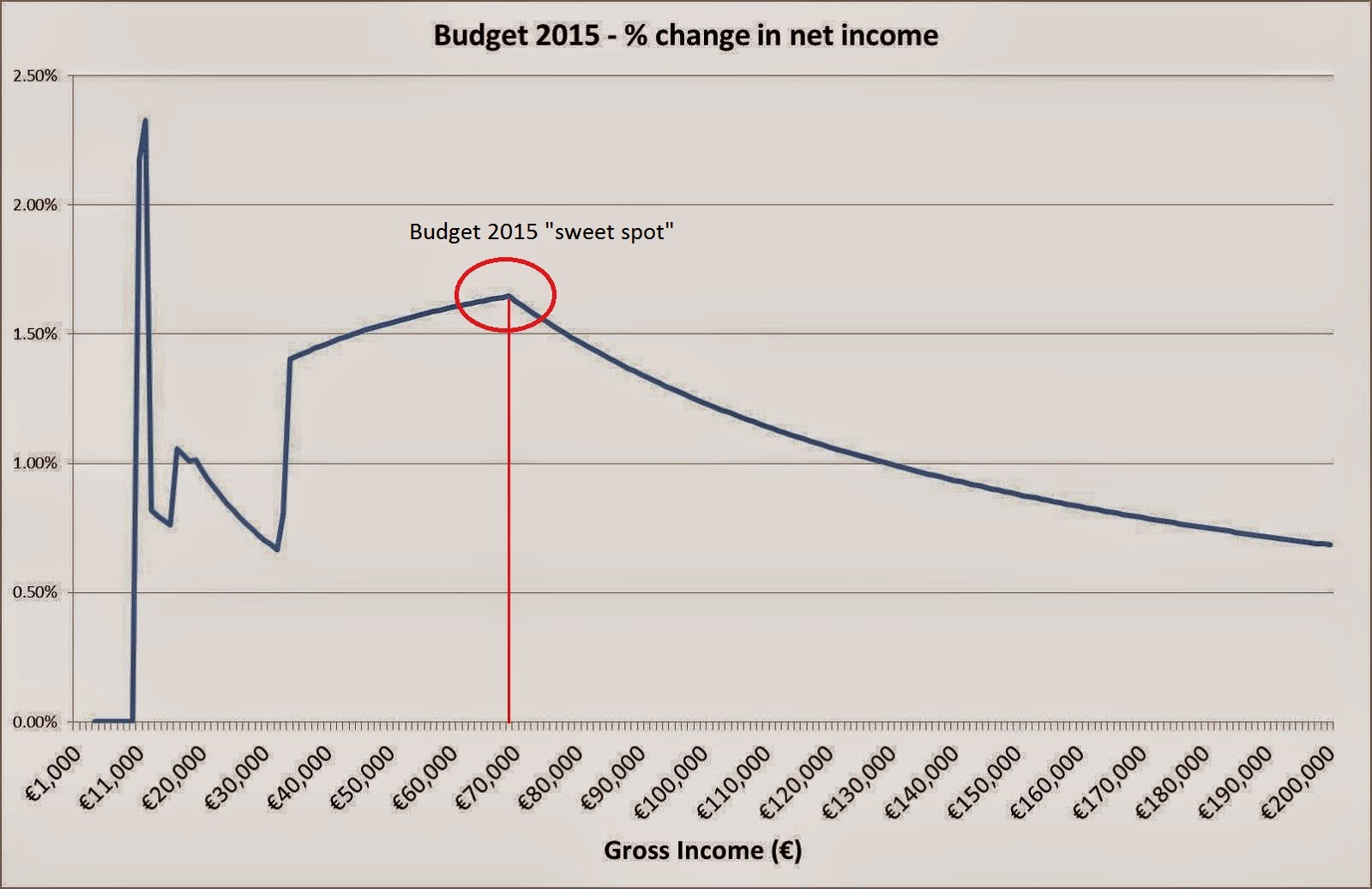

But the focus seems to be squarely on reducing the marginal rate on the group between €33,800 and €70,000. What we have seen from Budget 2015 is that cutting marginal rates for this group give the greatest benefit for those on the highest incomes (€70,000 and above), not those near the middle.

A tax benchmarking exercise would need to consider the entire range of taxes and focus on effective rates, not marginal. And it should also consider how we are going to fund our public services: which is why we raise taxes in the first place.

If the intention is to make Ireland the lowest tax country on all fronts (we already have the lowest social insurance in the EU) then we need to accept that we will also have the lowest public services.

Having minimal public services, which reduces the quality of life for everyone, is hardly a prospect that will entice young people to return home.

Cormac Staunton is Policy Analyst at TASC. You can follow him on Twitter @Cormac_Staunton

Cormac Staunton @cormac_staunton

Cormac Stauton is currently a policy advisor on EU and international policy in the Central Bank of Ireland. Prior to this, he was a policy analyst in TASC, and co-authored the first economic inequality report, Cherishing All Equally.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)