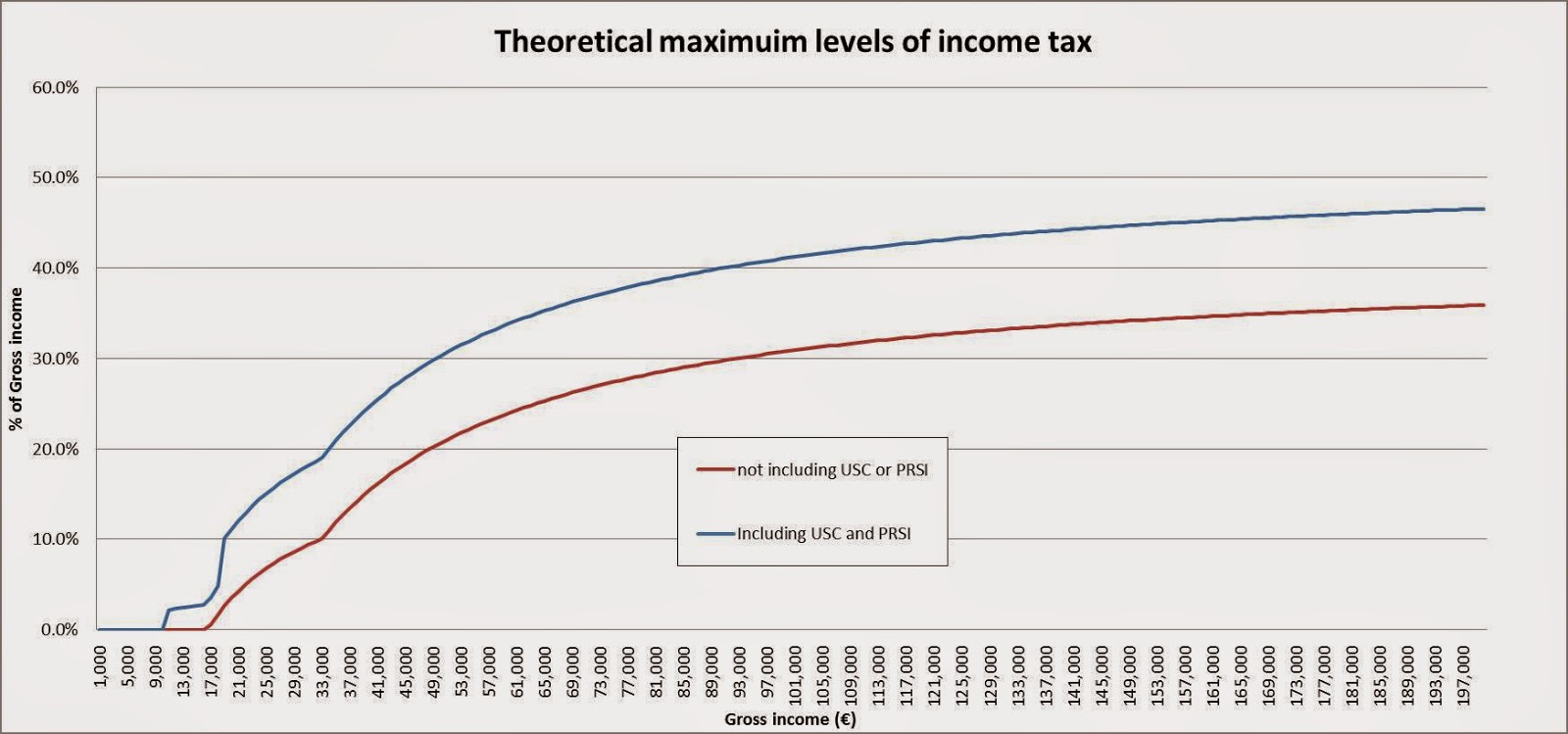

Cormac Staunton: TASC has previously shown how the progressivity of Ireland’s income tax system declines after certain levels of income. It is progressive (in that the percentage of tax paid increases as incomes increase) up to about €75,000 but then the relative progressivity begins to slow and then almost flat-lines.

See this diagram, which is based on tax liability as a percentage of income for a single person:

The red line is tax, the blue line is tax plus USC and PRSI. These are calculations of liability based on the rules, not actual tax paid (which we have shown to be lower).

The progressivity happens because someone on €18,000 has a liability of about 10%, and someone on €33,000 has a liability (tax, USC and PRSI) of roughly 20% of gross income. This rises to almost 40% for someone on €90,000.

However, for someone making a jump to €150,000, the rate only rises by a few percentage points to less than 45%. No one, even on extremely high income, ever pays more than half.

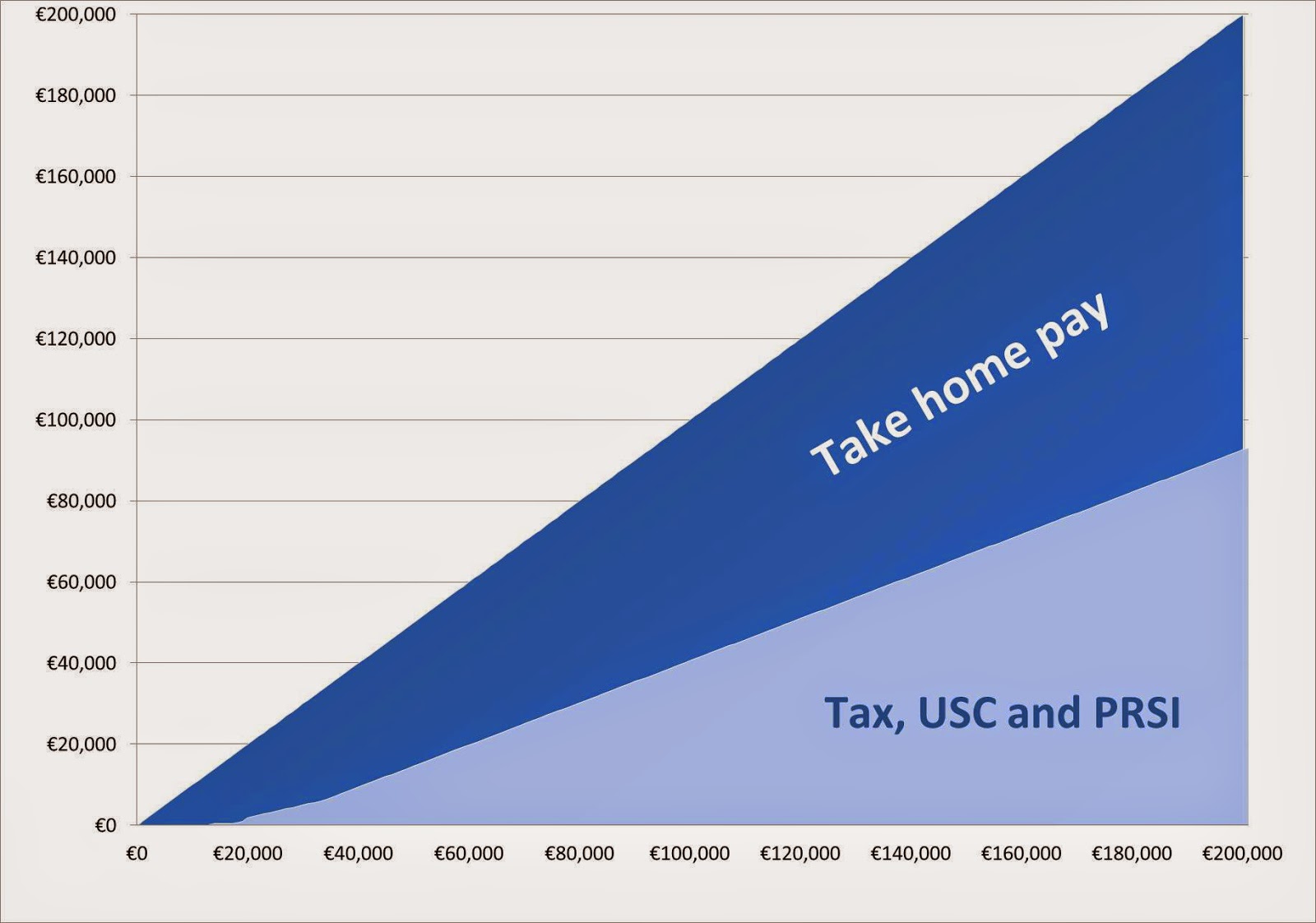

Another way of looking at it is to look at the tax liability in cash terms, and compare that to gross income. This can be compared to a plotted line of income tax, USC and PRSI. The diagram looks like this:

What this shows is that at all stages, the more you earn, the more you take home. There are no “diminishing returns” and no disincentives to work.

Cormac Staunton is Policy Analyst at TASC. You can follow him on Twitter: @Cormac_Staunton

Cormac Staunton @cormac_staunton

Cormac Stauton is currently a policy advisor on EU and international policy in the Central Bank of Ireland. Prior to this, he was a policy analyst in TASC, and co-authored the first economic inequality report, Cherishing All Equally.

Share: