Paul Sweeney: We will demonstrate why austerity is failing by looking at key economic indicators, with a focus on the most important indicator, employment, in the next post. The bailout package made economic recovery more difficult than it needed to have been. The level of the adjustment and the mix of the cuts and taxes (2:1) is wrong and should be reversed. The deflationary impacts of the measures in the package are such that growth has been negligible and this not largely due to the recession in Europe.

However, those economic factors which are positive will be examined first.

The deal on the Promissory Notes agreed on 7th February 2013 will be of significant benefit to Ireland. Secondly, the Government is on track to meet its fiscal deficit targets so far. The key and almost singular area of interest to the Troika is that Ireland meets its fiscal target of 3% by 2015. The Irish government has met all targets set out by the Troikas in each review since end 2010. To achieve this target €24bn has been taken out of the economy by end 2012 and a further €9bn will be taken out in the next three years. This is equivalent to cutting over a quarter of our GNP.

Thirdly, Irish exports are holding up and the Balance of Payment is in surplus. Exports are driving what little growth we have. After six quarterly declines to end 2009, exports have been rising. This is not a great achievement as Ireland’s exports are largely non-cyclical, being ICT, pharma and food. Labour costs in many exports are not significant. However, imports are down (by 25% from peak) as people have little to spend on them. The Balance of Payments are now healthy with a big surplus of exports over imports. But it is due in part to imports collapsing, due to lack of domestic demand.

A fourth positive factor is that the rate of interest on 10 year bonds is down and will stabilise after the deal on the Promissory Notes.

Productivity is also up substantially, i.e. unit labour costs were down by 23% since mid 2008 (real HCI) and this has been achieved without a fall in averaging hourly earnings for most workers (i.e. it was achieved without a painful internal devaluation for labour). Thus it is due to a) less people at work; b) better use of capital and labour; c) to the decline of low productivity construction and on the other side to d) the dependence on apparently high productivity multinationals, due perhaps in some measure to transfer pricing.

The fifth positive factor is that the Purchasing Managers index continued to rise. Sixthly, the level of inflation at end 2012 was slightly lower than it was in 2008. Prices fell by -4.5% in 2009 and again by a lesser -1% in 2010 but rose since then. Prices are rising by 1.2% now and are likely to pick up.

Moving from the positive to neutral we look at incomes. In spite of two cuts in the pay of all public servants averaging 14%, average hourly earnings in the total economy have not fallen in real terms. It was seen that the previous government tried an experiment in Internal Devaluation. It cut public service wages and the minimum wage by a massive 12%, expecting that private sector wages would follow.

This did not happen and private sector earnings have been relatively stable. About 24% of employees have had pay rises, c. 22% have had cuts and most have had no or little change in hourly earnings. The number of hours worked has dropped and so weekly earnings including overtime and other premium payments had fallen slightly. However, the latest data saw weekly earnings rise by 1.1% in the year to Q3, 2012. We have seen that productivity has risen substantially since the Crash of 2008.

A recent study of how employers dealt with the total wage bill found that there had been cuts, but “however, these cuts were primarily achieved though employment reductions with relatively low contributions at the aggregate level from changes in average hourly earnings and average weekly paid hours.”

This relative stability in real incomes of those who kept their jobs since the Crash of 2008 has also been extremely important in ensuing that the huge collapse in domestic demand – of one quarter in five years – was not worse. This is because averagely paid workers generally spend most of their incomes. The last government also cut the minimum wage by 12 per cent but the new government reversed this immediately. It also did not cut welfare rates and there is a deal with the public service whereby there will be no further pay cuts (two of which had averaged 14 per cent) provided there is support for substantial change, which is occurring.

These are all important indicators of performance, but others factors are far less impressive.

Economic Growth

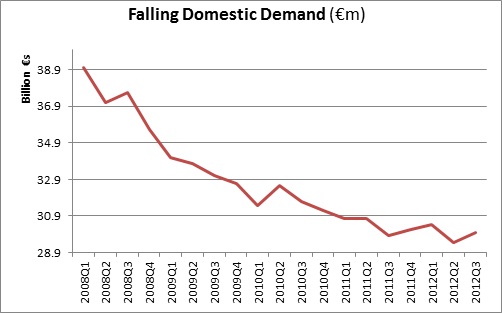

The economic growth figures, either GDP or GNP, have been scraping along the bottom for some years, which is better than the collapse. The next chart (Fig.1) shows the fall in domestic demand, which is so important for employment. It is still in decline.

FIGURE 1: Domestic Demand has COllapsed

Source: CSO, National Income A/Cs.

Most conservatives have focused on the one positive economic development which is the performance of Irish exports. Exports have performed very well, but exports alone are not sufficient to pull the economy out of recession when domestic demand is being driven down by domestic economic policies. Without growth there will be no new jobs. Without new jobs, generating incomes, taxation and confidence, the burden of austerity could overwhelm us.

The large gap between Ireland’s GNP and GDP is growing and rose from 14/16% to 27% of GDP. Thus GDP appears to be faring much better but it is a poorer indicator of welfare for Ireland.

A key part of the lack of demand is due to the flatness of wages. The reversal of the cut in the Minimum Wage did help. The government sought “reforms” of wage setting mechanisms the Employment Regulation Orders (EROs) and Registered Employment Agreements (REAs), and instructed the Labour Court to undertake the review with an academic economist who was to assess their impact on jobs. He found that most had minimum impact on jobs. So this dialogue was reasonable.

However, some of Ireland’s wealthiest employers in the fast food industry, the Quick Food Alliance , successfully fought a case to the High Court to abolish the Joint Labour Committee in the fast food industry and Employment Regulation Order of the Labour Court which had set the minimum pay and conditions of workers outside Dublin, as unconstitutional. The law courts are blunt instrument in dealing with industrial relations as the outcome is generally stark. The effect of the judgement is that while all JLCs remained in existence their EROs became unenforceable and ceased to apply. As a result the National Employment Rights Authority (NERA) could not enforce the minimum pay and conditions of employment prescribed in EROs in force at the time of the High Court decision. The Government amended the legislation in response to the court ruling. A review of the JLCs is taking place now and the unions await the outcome before they determine if the legislation meets the requirements of workers in these sectors.

Public and Personal Debt

The socialisation of the bank debt has pushed Public debt up and it was 118% GDP at end 2012 and will peak at around 121% in 2013. On top of high public debt, private debt is very high too. Household net worth has fallen by 37.7 per cent since the peak in Q2, 2007. Household debt is at €180bn or €39,999 per household. As a ratio of disposable income, it stands at 210 per cent thought it has reduced from its peak at 220 per cent in Q3, 2011.

Very Low Investment

A real worry must be the extremely low level of investment in Ireland. Total Irish investment is the lowest in the EU27 member states in 2012 at around 9 per cent of GDP compared to an average of 18.5 per cent. Ireland is even below Greece at 12 per cent. It may fall further in 2013 with the 2013 Budget cutting the Capital Programme by a further €0.55bn, though the Central bank thinks investment will begin to grow - but not until 2014. This very low level of investment in Ireland does not auger well for the future.

Paul Sweeney @paulsweeneyman

Paul Sweeney is former Chief Economist of the Irish Congress of Trade Unions. He was a President of the Statistical and Social Enquiry Society of Ireland, former member of the Economic Committee of the ETUC, a member of the National Competitiveness Council of Ireland, the National Statistics Board, the ESB, TUAC, (advisor to OECD) and several other bodies. He has written three books on the Irish economy and two on public enterprise, including The Celtic Tiger; Ireland’s Economic Miracle Explained and Selling Out: Privatisation in Ireland, chapters in other books and many articles on economics.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)