An Saoi: On Thursday 12/1/2012, Finance Minister Michael Noonan answered a series of questions on inheritances and Capital Acquisitions Tax.

The questions and the answers start here and continue over the next few pages of the Oireachtas website and provide a huge amount of detailed information on the subject of inheritances and gifts, but even more interesting is the information not provided.

The issue of estimating the tax yield has been fraught for many years. So in response to her question on the preparation of the estimate of CAT, Mr. Noonan advised that “… projections for capital acquisition tax receipts are not produced by reference to details of the numbers of deaths, gifts, property values, reliefs and exemptions.” It seems they stick a wet finger in the air, see which way the wind is blowing. Their general level of accuracy is reflected by their haphazard approach.

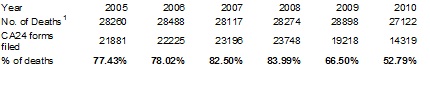

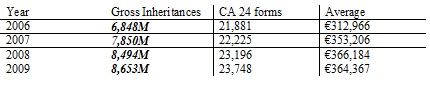

CAT appears to have a very low level of priority within the Revenue as the level of compliance in submission of Inland Revenue Affidavits (Form CA24) shows. As always, click to enlarge graphics.

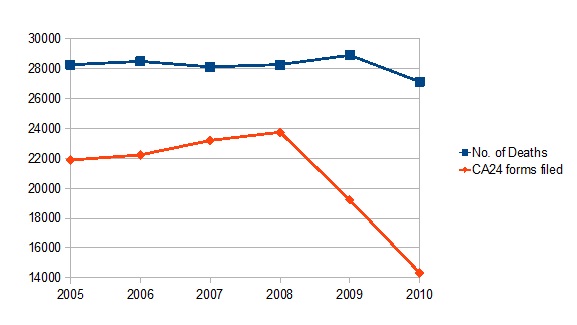

.. or perhaps the degree of the appalling job the Revenue is doing is better reflected in a graph:

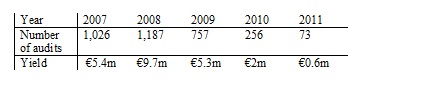

The Minister would not/could not provide details of the number of Capital Acquisition Tax audits that had taken place in recent years. Instead provided total figures for audits carried out under three headings, Stamp Duty, Pensions & CAT. Even then the numbers were appalling. However in the circumstances it is fair to say that no CAT audits have taken place in recent years.

It is time to move on to the meaty part – the figures.

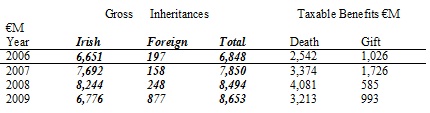

There are huge discrepancies between gross inheritances and taxable benefits taken at death with just 37.1% of the gross being taxable in 2006 & 2009 with higher figures in the intervening years. No reasons were given for the size of the difference.

The average size of estates where forms have been returned is calculated in the table below.

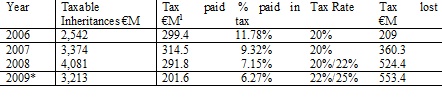

The Minister refused to provide any separate analysis of the number of gift returns made, perhaps because of the average size of gift and the degree of tax avoidance. However let us look at the average tax yield on benefits taken at death and (declared) gifts.

Taken at death

* I have used a composite rate of 23.5%

Gifts

The answers provided by the Minister raise as many questions as they answer. I hope that Joanna will follow through with some more questions in the near future to shine a further beam of light on this area.

The level of compliance is alarming. There is a lack of a clear picture of what is going on, nor any sign of a desire to tackle the issue. The percentage tax paid of (declared) gifts and inheritances is extremely low. There have been further slight amendments this year, but we don’t why or on basis those changes were made. Finally the level of openly admitted ignorance of Dept. of Finance is incredible, if not surprising.

Since the appointment of Dermot Quigley initially as a Commissioner and subsequently as Chairman of the Revenue, the organisation has certainly had the slickest PR & Media operation in the Public Service. Even the recent road bump over the pensioners was handled with panache by the current Chairman Josephine Feehily who wiped the floor with the Teachtaí in Committee Room 4 when called to account for her handling of the issue. I would be interested to see what she has to say about this CATastrophe.

Notes:

1. No of deaths for 2005 to 2008 are actual deaths in the year, for 2009 & 2010 it is the number of deaths registered.

2. Revenue Commissioners Annual Statistical Reports

3. Revenue Commissioners Annual Statistical Reports

Share: