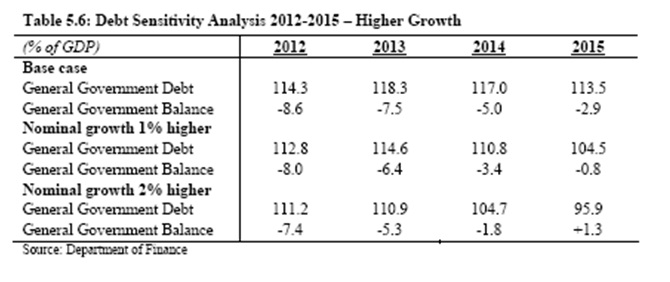

Michael Burke: Having criticised the government’s talk of improvement in government finances and the economy on the basis of the MTFS forecasts, the document does contain an important step forward. Apart from one small reference in a long-ago SPU, there has never been any official estimate of the sensitivity of government finances to changes in GDP. There is now.

This clearly shows that a 1% increase in GDP leads to a 0.6% improvement in government finances (as a % of GDP) in the first year (2012). An increase of 1% of GDP in the first year leads to a lower deficit from 8.6% of GDP to 8% of GDP. [This was what the earlier SPU said, which was strongly disputed by many, including Karl Whelan here.

But it gets better. The table also shows that for the 1% increase in GDP is an increasing sensitivity of government finances, 1.1% in 2013 rising to 2.1% by 2015. These are in effect the compounding effects of growth on government finances, as the level of GDP grows and both tax revenues and government outlays improve.

At the very least this vindicates the original assertion on the sensitivity of government finances which is crucial to the argument of all those who favour stimulus. That, first, government investment leads to much stronger growth and, second, that this stronger growth leads to much improved government finances (60 cents for every €1 increase in output in the first year, rising to €2.1 over 4 years).

It also points a way to resolving the crisis. Austerity is not only proving hugely damaging but is not delivering deficit-reduction. Growth can.

Share: