Tom McDonnell: The Greek tragedy that is the eurozone debt crisis may soon enter its fourth act. A hard write-down of Greek debt is necessary and there is now a significant probability that Greece will be allowed to default around December. Martin Wolf argues here that:

“the bare minimum the eurozone needs to cope with its crisis is an effective mechanism for writing down the debts of evidently insolvent private and sovereign borrowers, such as Greece; funds large enough to manage the illiquid bond markets of potentially solvent governments; and ways to make the financial system credibly solvent immediately.”

He suggests the sums required will be several times larger than the €440bn of the existing EFSF.

The Dexia crisis is finally forcing the core countries to acknowledge that their banking systems are in serious trouble and this creates an opportunity for Ireland. While the original intent was for the EFSF to be a sovereign bailout fund it is becoming increasingly clear that its future role will likely involve the recapitalisation of failing banks.

If and when Greece is allowed to default the EFSF will be standing by to preserve the solvency of the European banking system through large-scale recapitalization. It is at this point that the Irish Government should request the Anglo/INBS promissory note liabilities be transferred to the EFSF with Ireland then agreeing a negotiated repayment schedule at a low interest rate.

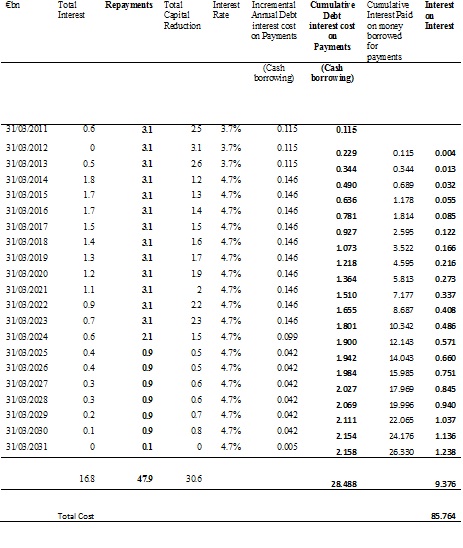

Renegotiating the promissory notes is of huge consequence to Ireland’s future prosperity. Michael Noonan hints here that he has begun the process of renegotiation. We can extrapolate from these new figures that the total cost between 2011 and 2031 will be in the region of €85 billion (assumes a 4.7% interest rate from 2013 onwards). That is €4 billion a year. The infinite spiral of cumulative interest costs is the reason why the figure is larger than the commonly cited €47 billion i.e., we have to pay interest on the €47 billion in borrowings and then pay the interest on the borrowings required for those interest payments and so on and so forth (click on table to enlarge).

Seamus Coffey explains the issues here. Turning the notes into a long-term bullet bond owed to the EFSF may offer one plausible solution. Our institutions were unforgivably unprepared for the 2008 earthquake. It would be feckless to sail in to the current storm without a worked out strategy to deal with the promissory note question.

Dr Tom McDonnell

Tom McDonnell is senior economist at the NERI and is responsible for among other things, NERI's analysis of the Republic of Ireland economy including risks, trends and forecasts. He specialises in economic growth theory, the economics of innovation, the Irish and European economies, and fiscal policy. He previously worked as an economist at TASC and before that was a lecturer in economics at NUI Galway and at DCU. He has also taught at Maynooth University.

Tom obtained his PhD in economics from NUI Galway.

Share: