Michael Burke: IBEC’s attack on the JLC wage setting mechanisms in order to drive pay lower is not simply morally indefensible. It is economically illiterate.

The attack on the JLC is simply the latest round in the battle to lower real disposable wages which has already seen pay cuts and ‘levies’ in the public sector, as well as increases in indirect taxes, which, because they are based on consumption, adversely hurt and disproportionately hurt the poor.

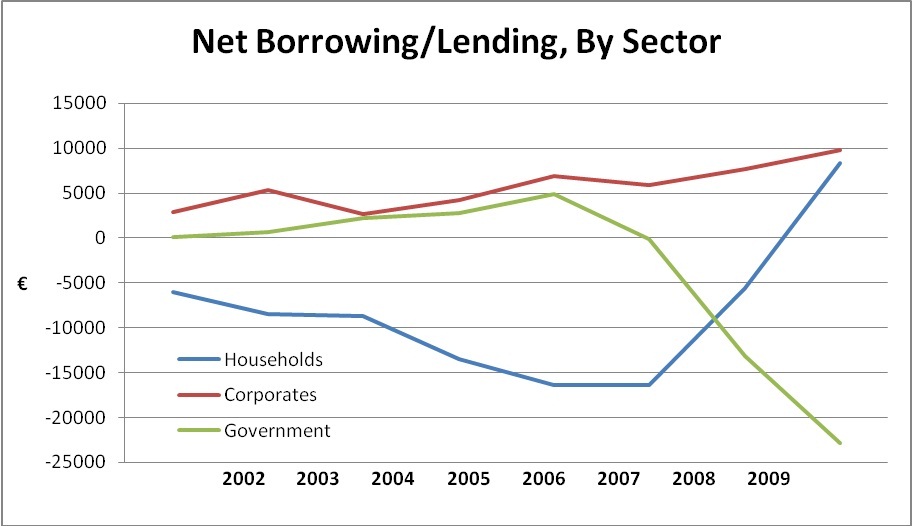

In any normally-functioning market economy the financial functions of the three main sectors are as follows:

*Households save some proportion of their net incomes

*Corporations borrow that savings for the purposes of investment (mainly via the mediation of the banks)

*Governments can run either a deficit or surplus, depending on the fiscal policy mix

(For the sake of clarity we’ll leave aside the role of borrowing from/lending to the rest of the world)

However, as the chart below shows, this economy has not been a normally-functioning one for some time.

Source: CSO

*Over a prolonged period (2002-2008) the household sector has been a net borrower

* For the entire period the corporate sector has not been a borrower but has been a net saver, and has significantly increased its savings in the economic slump

* Therefore, the government is obliged to become a net borrower, since all sectors cannot simultaneously be net savers.

At the sectoral level the source of the deficit is simply this fact- now that both the household sector and corporate sectors are net savers government is obliged to become a net borrower.

How to correct this imbalance? Policy has been to reduce the government borrowing by seizing a greater proportion of the household sector’s income (via taxes, pay cuts and reducing the government ‘s own investment).

But it has failed for two reasons. The household sector becomes more fearful (not more confident, as some of the wilder supporters of this policy have claimed) and so becomes even more inclined to save, not spend. At the same, the corporate sector seeing its two main customers (households and government) reining in their own spending has no need to increase its investment and instead increases its savings. The economy goes into a tail-spin and the government borrowing remains stubbornly high.

Alternative

What is the alternative? The household sector is supposed to be a net saver in a normally-functioning market economy. Now it is- even if the brutal manner in which that has been achieved has been highly damaging. But the corporate sector remains a large net lender, when it should be a borrower for investment. The slump in investment arithmetically accounts for the entire slump in the GDP of this economy. It is the corporate refusal to invest which both accounts for the slump and will prove hugely damaging to the economy over the long run- if it is not corrected.

At the same time, the existence of this corporate net lending belies entirely the notion that the economy is “broke”. The household sector may feel like it is broke. The government may be in danger of becoming broke, primarily because it insists on handing over money it doesn’t have to one part of the corporate sector; finance. But in 2009 the net income of the corporate sector was €38.8bn.

This is much reduced by the slump, but it is sitting idle – the corporate sector continues to be a net lender. Therefore to end the crisis the government should consider temporary measures to access these huge cash balances for investment purposes – taxes, levies, windfall payments and so on. These should be directed to key sectors of the economy which suffer a chronic investment deficit, infrastructure, rail, ports, broadband, health and education and so on.

The opposite course advocated by IBEC has already failed repeatedly. This is because it runs counter to the most basic tenets of economics. The investment of savings, primarily from households, is the key to future prosperity. Reducing those savings and reducing investment is to repeat the failed nostrums that caused this crisis.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)