Michael Taft: Some commentary has suggested that Black Thursday wasn’t all that bad; in particular the bail-out won’t add much to our general debt. Therefore (and this is a curious QED) the debt remains sustainable. Phew. I was worried there for a moment. In our own little bubble, we can content ourselves with the notion that our debt is ‘affordable, manageable and sustainable’.

It is difficult to say how much of the €24 billion bail-out will find itself in general government debt. Government sources claim only €2 billion – but even then, this depends on how Eurostat categorises the ‘expenditure’. So let’s factor in this marginal increase. What follows projects debt-to-GDP and GNP ratios – but this is not the only ‘sustainability’ measurement (the other measures interest rates, primary balances and growth).

If we use the last Government’s overly-optimistic growth (and, so, deficit) projections our debt will have to be revised upwards to 104 percent due to the poor 2010 GDP outcome.

However, let’s substitute the more sober IMF’s projections for growth and the deficit up to 2014. They project that growth will be an annual 2 percent; this contrasts with the last Government’s 2.7 percent; regarding the deficit, the IMF projects that the balance will be -5.1 percent; the last Government hoped to reach -2.9 percent (but that’s gone by the boards under the new Government).

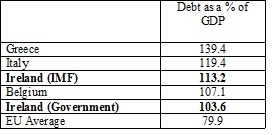

If we use the IMF’s projections, we find the Government debt rising to 113 percent by 2014. How does this compare to the IMF’s projections for EU countries by that year?

But let’s look at this from another perspective – debt as percentage of GNP (or Gross National Income).

If we take the Government’s optimistic projections, we’re still far in excess of the EU-15 average, coming second in the table.

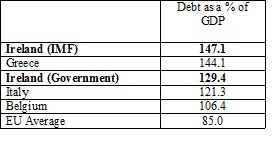

However, if the IMF projections hold, we will top the league – ahead of even insolvent Greece (note, however, that the Greek numbers will probably rise as their austerity programme is driving down growth and increasing the debt burden; just like Ireland).

With the markets convinced that Greece will default, how far behind can Ireland be? And this assumes that not one extra cent, as Minister Leo would put it, finds its way on to the state books. What odds on that not happening?

But even though we may be heading towards Greek levels of debt, we won’t have to worry. It will all be ‘affordable, manageable and sustainable’.

Just as long as we keep cutting (and cutting and cutting) social welfare, public services and investment.

Michael Taft @notesonthefront

Michael Taft is an economic analyst and trade unionist. He is author of the Notes of the Front blog and a member of the TASC Economists’ Network.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)