Nat O'Connor: The interest rate on the EFSF loan is to be 5.8 per cent (on average). Can Ireland afford this?

Professor Morgan Kelly of UCD wrote an opinion piece on 8 November 2010, where he spelled out his analysis that the Irish economy has passed the point of no return. His analysis hinged on the fact that the cost of the bank bailout in Ireland has been too expensive. He concluded his article by saying he could think of “no solutions”.

When it comes to the banking situation, Professor Kelly may indeed be right. The burden of servicing the bank bailout may be possible on a year-on-year basis, and even this is not sure, but the real task is to pay back that debt. Faced with this stark reality, there may be no option but to consider the renegotiation and partial write-down of that debt – which emanates from private sector decisions. Lenders should fully face the consequences that bad investments are meant to face in a capitalist, free market economy (as they are not shy about taking all the rewards in good times). In this case, that means a major write-down for the bank bondholders, as an alternative to several generations of Irish people struggling to pay back billions.

Professor Kelly’s prognosis must also cause us to consider – in an empirical and analytical way – the even more daunting political possibility of further default, of sovereign debt.

In terms of this kind of analysis, however pessimistic he may have felt, Professor Kelly did remind us of a “simple rule” that economists use to gauge whether national debt levels are sustainable or not: “If the interest rate on a country’s debt is lower than the sum of its growth rate and inflation rate, the ratio of debt to national income will shrink through time.”

The ratio in question is that nominal growth plus the 'primary budget balance' (as a percentage of GDP) must be higher than the rate of interest. Nominal growth is real GDP growth plus the GDP deflator - i.e. the effect of inflation. And the primary budget balance is the Government's balance.

Put more simply, nominal growth plus the Government's balance (surplus or deficit) must exceed debt interest payments. This is a long-term trend indicator. Obviously, if the Government has a surplus (more revenue than spending), it can absorb a couple of years of low growth. But as we have a deficit, a couple of years of low growth mean that we have to tax more or cut spending just to pay the debt interest and in addition to other taxes and cuts, which are to close the deficit. In the long-term we can't tax or cut forever, so we need to ensure our debt levels are sustainable. 'Manageable' if you prefer. And if our debt payments are not sustainable, we are just sinking further and have no hope of paying off the debt itself.

As a 'thought experiment', we can do a simple analysis using this formula, to see whether it is in fact possible for Ireland to overcome the debt mountain, if the right economic policies are pursued.

Note: to avoid confusion, debt interest is now being examined in two different ways. There is the rate charged on a particular bond or loan (such as the 5.8 per cent on the €85 billion loan) But we are also expressing debt interest for the year in question, which is the interest payments as a percentage of the total national debt.

We have nominal GDP figures from the Department of Finance and CSO for the past (e.g. CSO National Accounts), and we can use these to illustrate whether Ireland's debt was on a sustainable path.

It looks like 2007 was the last year where nominal growth exceeded debt servicing costs. In that year, real GDP grew by 5.6 per cent and the GDP deflator was 1.1 per cent; total 6.7. The interest cost of paying back our debt in 2007 was relatively. The debt was only €38 billion then, so debt repayments at were clearly smaller than 6.7 per cent of GDP. We had a surplus that could be used to pay off part of the national debt (shown here). That is, Ireland was in a sustainable position to pay the national debt.

Then came the recession. 2008's real GDP growth was -3.5, with a deflator of -1.5; total -5 per cent. Ireland's annual cost of paying debt interest was relatively low at this point. National debt was still low (at €38 billion) and repayments were €2.1 billion. But any level of payments obviously exceeded the negative nominal growth. The debt is never unsustainable during a year of negative growth, and so adds to the deficit.

2009 was worse. It was another year of negative nominal growth (-11.6). The debt was unsustainable in that year too. Similarly, the continued decline in 2010 (-2.9) makes it the third year in a row where servicing the interest on the national debt is significantly higher than nominal GDP growth. So debt servicing is adding to the deficit in these years.

If this is sounds too complex, David McWilliams also explains growth versus debt payments about halfway down this article.

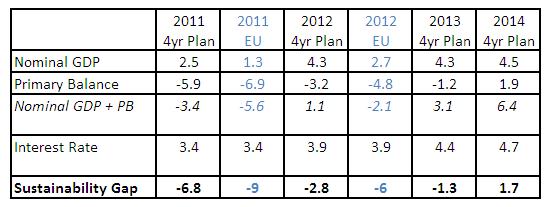

Looking forward, the four-year plan gives a table of numbers we need to make the same calculations for 2011-2014. Table A.3.1: Debt-Deficit Dynamics – The Baseline Scenario (p.107).

But the European Economic Forecast (29 Nov 2010) gives less optimistic forecasts of Irish growth than the Government's four-year plan.

The following table puts these figures together:

In 2011, Ireland will begin to draw down funds from the €85 billion loan. Our national debt interest rates will not suddenly shoot up to 5.8 per cent, because only a part of our national debt will come from this source. The larger part will be existing debts, which are at a total average fixed interest rate of considerably less. As we draw down more and more of the €85 billion, the annual interest rate will rise towards 5 per cent or more.

Not only has the interest rate risen, but it is 5 per cent of a larger debt, estimated at 102 per cent of GDP in 2011 (in the Government's four-year plan, p.108). 5 per cent of c. €160 billion (GDP in 2011) is €8 billion in debt servicing costs.

To cut a long story short, Ireland's debt is not viable in 2011. We will continue to have to tax and cut to find the money to pay the debt interest.

As the table shows, the situation in 2012 and 2013 is also poor, with debt interest payments adding to the deficit and national debt, even as we try to bring tax revenue and other spending into line with one another.

The four-year plan's growth figures show Ireland's debt becoming sustainable in 2014. On the face of it, this makes sense. Taxation and spending will (in theory) be brought into line with one another. However, debt interest will take up a large part of the spending - squeezing out health, education, welfare, capital and other spending.

The numbers add up, but are the numbers sound?

The EU's growth predictions for 2011 and 2012 are more sobre. If they represent a trendline of more modest growth, than the debt will still be unsustainable in 2014, and possibly for years to come. And every year that the debt interest is too much, it adds to the national debt and future years (higher) debt interest payments.

Over the same years, the fixation on the deficit, without serious investment in growth, will lead to a weakened economy.

To add insult to injury, the ECB's central mission is to keep inflation low. A dose of inflation would do no harm to Ireland right now, as long as that included wage inflation across the board. If the cost of living and wages both rose by 10 per cent, there would be no major change for most people - except that our debts would have shrunk relative to our earnings. Unfortunately, the monetary policy lever to bring about inflation is quantitative easing (printing money), which the ECB controls. There is a downside of course, savings would also decline relative to prices and incomes.

Alternatively, another bubble in the economy is not a good idea; slower, steadier growth is what's needed. And a high inflation component isn't likely, because the ECB won't let it happen.

The Government is holding out the possibility of a return to the bond markets to borrow money at less than 5.8 per cent, as soon as we can. But the financial institutions who lend to states can do a more sophisticated analysis than I have just done. They see the unsustainability of the level of debt; and so bond yields are likely to remain stubbornly high.

As TASC has continued to point out, there is a sympathetic relationship between economic growth and the bond markets. If the Government can lay out a credible strategy to restore the Irish economy to a growth trajectory, then the bond markets in turn will have more confidence that Ireland will be able to pay back its debts and yields will lower accordingly. The Government's strategy of austerity has not, to date, included a growth plan. They have simply focused on the deficit, without enough attention to the wider economy – which at the end of the day is the 'engine' that provides both tax revenue and overall GDP.

So, measures to boost growth would seem to be an obvious requirement. Except that the terms of the €85 billion loan limit our options by sacrificing most of the pension reserve fund.

In the absence of pan-European co-ordination on emergency monetary policy measures, which may be ultimately required to save the euro, Ireland has to take major decisions on its own. Only a combination of radically restructuring our national debt (i.e. defaulting on the banks' debt) and a jobs strategy with serious money invested in it (e.g. the NPRF) will generate the growth that is required to have the ability to pay our already high national debt (not including the bank debt).

The €85 billion deal, at 5.8 per cent, is too expensive. Didn't the Government put new 'inability to pay' clauses into the four-year plan?

Dr Nat O'Connor @natpolicy

Nat O’Connor is a member of the Institute for Research in Social Sciences (IRiSS) and a Lecturer of Public Policy and Public Management in the School of Criminology, Politics and Social Policy at Ulster University.

Previously Director of TASC, Nat also led the research team in Dublin’s Homeless Agency.

Nat holds a PhD in Political Science from Trinity College Dublin (2008) and an MA in Political Science and Social Policy form the University of Dundee (1998). Nat’s primary research interest is in how research-informed public policy can achieve social justice and human wellbeing. Nat’s work has focused on economic inequality, housing and homelessness, democratic accountability and public policy analysis. His PhD focused on public access to information as part of democratic policy making.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)