Rory O'Farrell: What is the bottom line for the Irish economy?

It is well known that the economic bubble was inflated by borrowed money, largely in the private sector. What is largely being ignored is that the total economy, public and private sector, is still being financed from abroad.

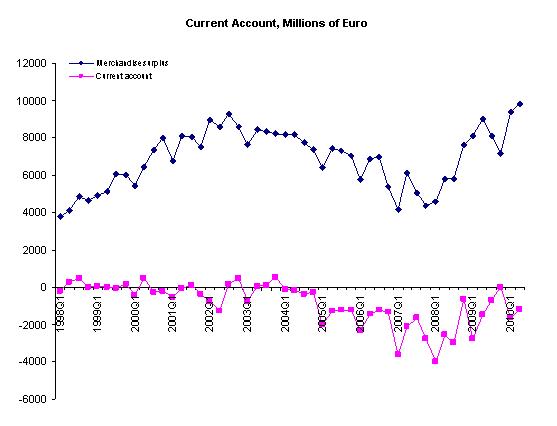

Ireland has successfully managed a trade surplus in our recent history, exporting more than we import. We have had a steady income. However, for most of the 21st Century we have shown a Current Account deficit. But why is this important? The Current Account in the National Accounts in many ways is similar to the current account a private citizen has in a bank (it is complicated in that it measures flows rather than stocks). It measures the day to day items of the national economy. It includes our trade balance, but crucially for Ireland, it includes some of our day to day expenses in the global economy. Each quarter the Irish economy must send money abroad to pay interest bills and the profits to multinationals. Given our liabilities, Ireland has to run very fast to stay still. Even having a trade surplus of €10 billion may not be enough push us back in the black.

Though the fiscal deficit is important, the Current Account serves as the bottom line for the economy as a whole. If we want to pay back our private sector debt (such as in Anglo or AIB) without just lumping it onto the National Debt, we must show a Current Account surplus.

What can be done?

It is inevitable that our debt overhang will resolve itself eventually, but as with everything in economics there are choice as to how to deal with the issue. Continuing with government policy will lead to debts being resolved through bankruptcy.

The most obvious way to reduce out international liabilities would have been to allow private sector debt stay private, and allow the bank bondholders take a hit. This would have been the correct thing to do. Unfortunately this is getting more and more difficult to do as the Government added private debt to the public debt.

We can increase exports. Unfortunately this is difficult, though not impossible. We cannot change demand from abroad but we can make ourselves more competitive.

One suggested way is to lower wages. However how would this benefit the current account? It might increase inward investment in the medium term, but as wage rates are already competitive it is unlikely it would have much of an effect. Also, as our export sector is dominated by multinationals cutting wages would simply increase the profits that are sent abroad, so a wage cut could actually harm our Current Account position. Alternatively we could try reduce non-wage costs by investing in public infrastructure.

We can reduce imports. This is something we have far more control over. One possible way is through massive Government cut backs to kill off domestic demand for imports. This is a strategy that was pursued by the IMF in South America, but they have moved away from this. The social consequences are too severe. Also a social wasteland does not make for a good export platform, so such a tactic could also reduce exports, and not improve the Current Account balance. As most government spending is done domenstically. There is some leakage abroad, but government spending can be targetted in a way to minimise this.

The government could look at which income groups spend the most on imports and increase their income tax rather than that of other groups. Also Ireland imports a disproportionate amount of goods, mainly due to our dependence on foreign energy. Investing in alternative energy is a good substitute, but also the simpler solution of public transport and cycle lanes would reduce the amount of fuel we import.

Finally we can reduce capital outflows and have one big inflow. Repatriating the National Pension Reserve Fund would be the obvious inflow. But what of outflows? Saving does not always equal investment. We should look at which income groups save their money abroad and tax them more. This will help to keep money in the domestic economy, and reduce our external liabilities.

It may be argued that this policy is protectionist, but we simply cannot afford to keep importing at the rate we have been.

Dr Rory O'Farrell @r_o_farrell

Rory O'Farrell is an economist lecturing in TU Dublin. He previously worked for the OECD and for NERI.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)