Michael Taft: Conor McCabe has produced an interesting and potentially disturbing set of figures over on Dublin Opinion. Based on World Trade Organisation data, he compares the exports per worker in the financial sector in the following countries:

Spain: $23,398

Italy: $15,492

Netherlands: $38,182

The figure for Ireland is, however, an astronomical $367,033. He goes on to ask whether these figures are based on a fiction – the same fiction we were fed only a few year ago:

‘Do you remember holiday homes? How every single unsold house in Ireland was a holiday home so there was nothing to worry about? That there was no bubble? In fact, we should keep on buying homes at inflated prices because there were no inflated prices? All those reports in the newspapers, all that property porn on RTE? We were told not to worry, that the purchases were real?’

So are the figures for Irish service exports this year’s holiday homes? We have to be cautious. One explanation could be that the Irish financial sector is more export-oriented than other EU countries which are dominated by home market activities – especially considering the presence of our IFSC. Still, an export of more than 10 times per other EU workers seems a tad on the high side.

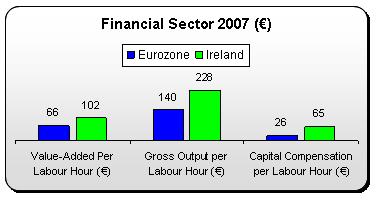

The issue isn’t academic. If we are to have an ‘export-led recovery’ we must be confident that we can accurately measure those exports and that such measurements are robust enough to base future policy on. This calls for a critical approach that goes beyond the surface of headline figures. Are there other ways to compare our financial sector with other EU countries? Yes, courtesy of the EU Klems database. These comparisons mirror Conor’s figures:

We see that value-added per labour hour in the Irish financial sector is over 150 percent that of the Eurozone average; gross output is over 160 percent; while capital compensation – or profits (gross operating surplus) – is 250 percent of Eurozone average. Are these numbers credible? Or are we picking up something else – namely, transfer pricing activities (whereby the profits generated in other countries are counted as part of our GDP)?

Even if these numbers are capturing real economic activity, there are other reasons to be cautious about what the Central Bank Governor calls the ‘dynamism of Irish exports’. According to the CSO, financial/insurance exports increased by 47 percent between 2003 and 2007. During that same period employment increased by 17,000 jobs – or 4,250 on average.

The question is, will these exports return to that growth – a growth stimulated by a regime of financialisation that now seems like from another age; an age not plagued by credit constraints and substantial deleveraging? If anything, we may be heading into a period of considerable employment contraction if the IBOA’s fears are even partially realised.

And that’s if the exports figures are all above board.

Conor has opened up a new area of investigation and consideration. It’s about time we took a cold, hard look at some of the platitudes and easy assertions that pass for informed comment. Otherwise, we may end up with more empty assets, bankrupt policies and a future where recovery is statistical only.

Michael Taft @notesonthefront

Michael Taft is an economic analyst and trade unionist. He is author of the Notes of the Front blog and a member of the TASC Economists’ Network.

Share: