Michael Taft: Strange how some things don’t get into the debate. For instance, the ESRI’s recent Recovery Scenarios judged the Government’s fiscal strategy a failure. It estimated that not only will the Government fail to bring public finances under control by 2014 (if we take the Maastricht guideline as the ‘control’ threshold), it will not be able to do so by 2020. Did any of this get into the debate? Were there discussions on the failure of spending cuts? No. The debate is impervious to such awkward interventions. Spending cuts are good. No amount of reality will be allowed to perturb the consensus.

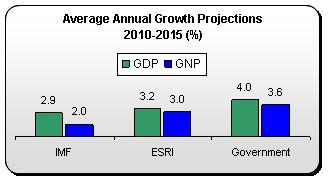

The ESRI presented two growth scenarios for the Irish economy – high-growth and low-growth. In reality, the low-growth scenario is more likely for the simple reason that it is not really ‘low’. It’s lower than the Government’s projections (which have been labelled ‘optimistic’ by the IMF and the OECD) but higher than the IMF estimates. So it’s pretty much in the mid-range.

On the basis of this low-growth scenario, the ESRI says the Government cannot reach the Maastricht threshold – not by 2014, not by 2015 not even by 2020.

• By 2015 the deficit is estimated to be 4.1 percent (not counting any banking subsidies)

• By 2020 the deficit is estimated to be 4.5 percent

In addition, they estimate our overall debt levels will be 102 percent of GDP in 2015, rising to 106 percent five years later.

The reason the deficit and debt start rising after 2015 is because the ESRI estimates that real growth will start to ease off, falling from an average 3.2 percent over the next five years, to 2.1 percent afterwards. On this basis, we would have to cut the deficit to well below -3 percent by 2015, just to ensure we don’t rise above it again in a few years. They summarise the problem:

‘The lower level of economic activity would reduce government revenue from taxation while the higher unemployment rate and borrowing would increase government expenditure on welfare payments and interest payments. This would result in a significant deterioration in the general government balance . . ‘

So why, according to the ESRI, would this state of affairs come about? They first assume the economy won’t respond to increased world growth as robustly as in the past. But they also point out that a poorly functioning banking system, higher cost of capital and structural unemployment could also contribute to a low-growth scenario.

What they don’t mention is the impact of the Government’s deflationary cuts - which is strange since they point out that the Government’s €3 billion fiscal contraction in the 2011 budget will cut economic growth (by approximately 1 percent – though this was before the Government’s announcement that spending cuts, which are more deflationary, will play a more prominent role in the composition of the contraction).

It is even stranger since they have just released a revised set of fiscal multipliers, updating their paper from last year. These updated multipliers show that they previously under-estimated the impact of spending cuts on economic growth:

• A €1 billion cut in public sector wages will reduce GNP by 0.4 percent (previously it was 0.3 percent)

• A €1 billion cut in public sector employment (about 17,000 jobs) will reduce GNP growth by 1.0 percent (previously t was 0.9 percent)

These might seem marginal but given the scale of cutbacks the Government (€2.4 billion in pay cuts, €3.6 billion in non-wage consumption, €2.6 billion in investment cuts), it all adds up.

The key metric is employment and this, more than anything else, helps explain the low levels of growth and, so, the failure of the Government’s fiscal policy. The ESRI estimates that employment will grow by an average 1.3 percent between 2010 and 2015. This compares to the Government’s estimate of 2.0 percent average.

Again, this might not seem much but add it up. But by 2015, the ESRI is estimating we will have approximately 70,000 fewer jobs than the Government’s projections. When you factor in the impact on tax revenue, unemployment costs and the significant social costs of long-term and structural unemployment – you start to see why the Government’s fiscal strategy will fail.

None of this should come as any news – if we were fortunate to get the news: the IMF similarly projected the Government’s fiscal strategy will fail. So, too, did the Ernst & Young / Oxford Economics report (though they held out hope that the deficit might come under control by 2018/2019 – but only at growth rates that exceed the ESRI’s estimates).

Of course, some might be tempted to say, that after nearly €9 billion of spending cuts with the prospect of billions more planned, all we need to do is cut just that little bit more. Just dig a little deeper and we’ll get out of the hole. But that’s the problem – every new estimate, every new projection tells us that fiscal consolidation is getting further and further away the more we cut. How much longer do we go along with this ‘Boxer mentality’ in the face of an emerging consensus that the Government’s strategy is flawed at its core; that no amount of tweaking will rescue it. Indeed, further cuts, in addition to what the Government is planning, will only undermine economic and employment growth even more. What will we do then? Call for even more cuts? How deep does the hole have to get before we stop digging?

So what have got? Low growth, escalating debt, high unemployment and emigration, sluggish economy – and the failure to repair public finances; if the ESRI buried the Government’s fiscal consolidation strategy, it also buried the McCarthy report. You probably didn’t hear about that either.

That’s why my next post will deal with that.

Michael Taft @notesonthefront

Michael Taft is an economic analyst and trade unionist. He is author of the Notes of the Front blog and a member of the TASC Economists’ Network.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)