Michael Burke: Paul Krugman, writing in the New York Times, asks whether fiscal austerity measures actually reassure the financial markets. This question is of course extremely pertinent to this economy. Not only has the FF-led government led the way in slash&burn economics in Europe, but this has become a defining totem of its economic policy - that the cuts are necessary to reassure financial markets.

Government policy was recently commended by the Wall Street Journal, and duly got a widespread airing. Krugman's analysis is very different and by implication much more critical of policy. I'm guessing his piece will get much less of an airing on the radio shows and might not be reproduced by the Irish Times. Just a hunch.

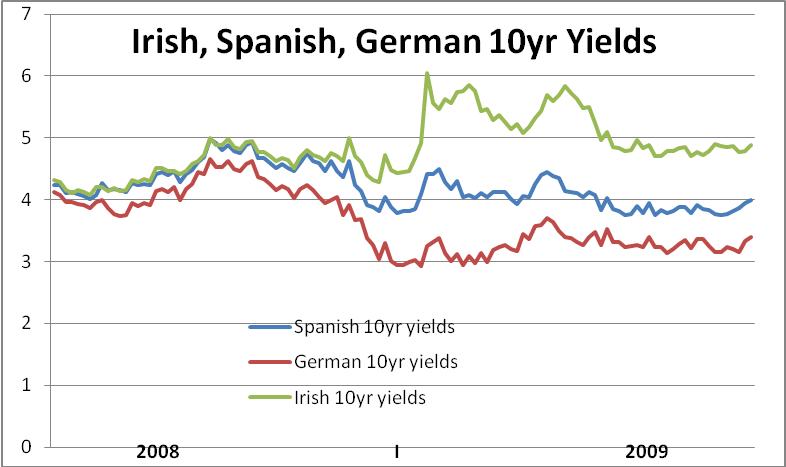

But who is right, the WSJ, or the NYT's Nobel-winning economist? The only way to judge is in their treatment of facts. Specifically, both articles refer to the reaction in the bond market to Dublin's economic policy, and the contrast with that of Madrid. Krugman points out that Irish 10yr bond yields are higher than Spanish ones, despite the fact that the latter had to be recently strong-armed into fiscal austerity and there has been a public backlash against the measures. He also points that Irish Credit Default Swap rates are higher than Spanish ones. Although these are less reliable guides than bond yields, because they are smaller, more illiquid markets, they do indicate that more speculators are betting on an Irish default than on a Spanish one. Helpfully, Krugman provides links to Bloomberg charts, so the facts at least cannot be contested. In neither case can it be argued that the fiscal austerity here has provided greater reassurance to the markets.

But what of the Murdoch-owned WSJ? It certainly uses lots of facts to support its argument that policy here is correct, and should be emulated. But how it uses those facts is less than rigorous.

To take the key area of disputed ground, bond yields, this is what the WSJ says in its opening paragraph, "SPANISH TWO-year government bond yields climbed five basis points to 2.47 per cent on Monday morning, after Fitch last week cut Spain’s triple-A credit rating to double-A-plus. Ireland, on the other hand, has been making do with its diminished Fitch rating of double A-minus since November. And yet yesterday morning the yield on its two-year government bond was at 1.77 per cent, down seven basis points from the day before, though its 10-year yields remain elevated." The full piece can be read here.

It is perfectly true that Spanish 2-year government yields are higher than Irish ones. But the WSJ article glossed over the fact that Spanish 10-year yields are significantly lower as they have been throughout the crisis. This is shown in the chart below.

Yields

10-year yields are the accepted benchmark for government debt, as prudent government borrowers attempt to lengthen the maturity of its debt precisely to avoid being hurt by wild short-term swings in market sentiment. Less than 20% of government debt is held at short-term maturities like 2 years, the bulk held at much longer maturities. So, while the WSJ treated us to a daily commentary on Irish 2yr yield movements, it passed over a key fact; that Irish long-term yields are higher than Spain's where it counts, which is where most of the borrowing is done. The grudging admission was that Irish 10yr yields 'remain elevated'.

All the crisis-hit countries in Western Europe, Greece, Spain, Portugal and Italy are suffering a fate that has already befallen Eastern Europe. International bodies such as the ECB, European Commission, IMF, etc. insist on austerity policies to reassure financial markets. Sometimes local governments are happy to oblige, others need arm-twisting. But the austerity doesn't reassure financial markets, so more of the same is demanded, and yields rise because bond investors think that the risk of default is rising, as Krugman points out.

Within that general trend, there seem to be favoured countries and not so favoured ones. These are the ones under attack and whose 2year yields are pushed higher as governments find it hard to access short-term funds. But it seems to have little to do with deficits- Italy's deficit is expected to be 5.3% of GDP this year the same as Belgium's, compared to 8% for France and 11.7% for Ireland. And it seems to have precious little to do with debt levels either, with Spain's debt at 64.9% of GDP this year, compared to 77.3% for Ireland, 78.8% for Germany, 83.6% for France, and 99% for Belgium. It does have a lot to do with the scale and foreign assets of each country's banking system, but that's another story http://socialisteconomicbulletin.blogspot.com/2010/06/parasite-threatens-host-impact-of.html .

Irish 10yr yields were the highest in the EU for most of 2009, as austerity was being implemented, in contrast to the rest of the Euro Area, where various types of stimulus measures were attempted. The reassurance that bond investors need is that you can meet interest payments and repay debt as it falls due. For governments that can only come from tax revenues.

Krugman ends with a question, should you believe what everyone knows, or your own lying eyes?

Share: